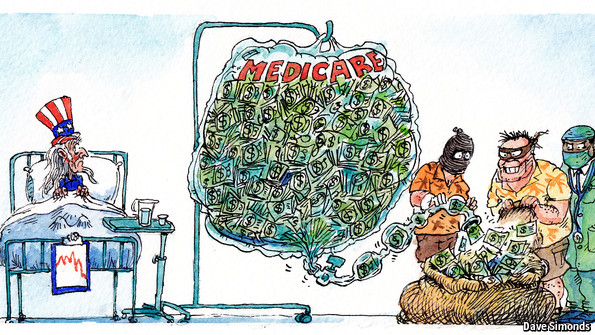

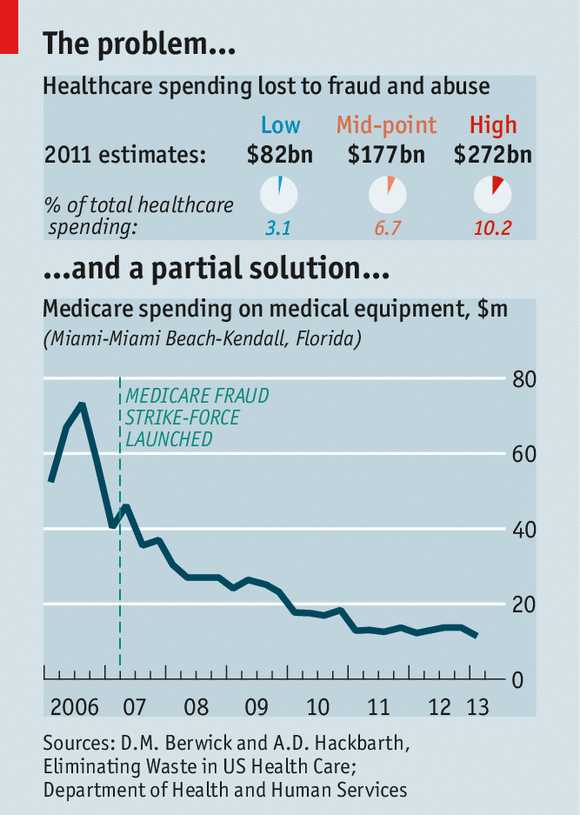

Will be useful to plug this into our health market quality explorations…

PDF: Digitizing the consumer decision journey McKinsey

http://www.mckinsey.com/Insights/Marketing_Sales/Digitizing_the_consumer_decision_journey?cid=DigitalEdge-eml-alt-mip-mck-oth-1406

Digitizing the consumer decision journey

In a world where physical and virtual environments are rapidly converging, companies need to meet customer needs anytime, anywhere. Here’s how.

June 2014 | byEdwin van Bommel, David Edelman, and Kelly Ungerman

Many of the executives we speak with in banking, retail, and other sectors are still struggling to devise the perfect cross-channel experiences for their customers—experiences that take advantage of digitization to provide customers with targeted, just-in-time product or service information in an effective and seamless way.

Video

How consumer behavior keeps changing

McKinsey’s David Edelman explains how purchasing decisions are made in a digital world.

This quest for marketing perfection is not in vain—during the next five years or so, we’re likely to see a radical integration of the consumer experience across physical and virtual environments. Already, the consumer decision journey has been altered by the ubiquity of big data, the Internet of Things, and advances in web coding and design.1 Customers now have endless online and off-line options for researching and buying new products and services, all at their fingertips 24/7. Under this scenario, digital channels no longer just represent “a cheaper way” to interact with customers; they are critical for executing promotions, stimulating sales, and increasing market share. By 2016, the web will influence more than half of all retail transactions, representing a potential sales opportunity of almost $2 trillion.2

Companies can be lulled into thinking they’re already doing everything right. Most know how to think through customer search needs or have ramped up their use of social media. Some are even “engineering” advocacy—creating easy, automatic ways for consumers to post reviews or otherwise characterize their engagement with a brand.

Yet tools and standards are changing faster than companies can react. Customers will soon be able to search for products by image, voice, and gesture; automatically participate in others’ transactions; and find new opportunities via devices that augment their reality (think Google Glass). How companies engage customers in these digital channels matters profoundly—not just because of the immediate opportunities to convert interest to sales but because two-thirds of the decisions customers make are informed by the quality of their experiences all along their journey, according to research by our colleagues.3

To keep up with rapid technology cycles and improve their multiplatform marketing efforts, companies need to take a different approach to managing the consumer decision journey—one that embraces the speed that digitization brings and focuses on capabilities in three areas:

- Discover. Many of the executives we’ve spoken with admit they are still more facile with data capture than data crunching. Companies must apply advanced analytics to the large amount of structured and unstructured data at their disposal to gain a 360-degree view of their customers. Their engagement strategies should be based on an empirical analysis of customers’ recent behaviors and past experiences with the company, as well as the signals embedded in customers’ mobile or social-media data.

- Design. Consumers now have much more control over where they will focus their attention, so companies need to craft a compelling customer experience in which all interactions are expressly tailored to a customer’s stage in his or her decision journey.

- Deliver. “Always on” marketing programs, in which companies engage with customers in exactly the right way at any contact point along the journey, require agile teams of experts in analytics and information technologies, marketing, and experience design. These cross-functional teams need strong collaborative and communication skills and a relentless commitment to iterative testing, learning, and scaling—at a pace that many companies may find challenging.

Let’s consider what an optimized cross-channel experience could look like when companies target improved capabilities in these three areas.

A new normal …

Imagine that a couple has just bought its first home and is now looking to purchase a washer and a dryer. Mike and Linda start their journey by visiting several big-box retailers’ websites. At one store’s site, they identify three models they are interested in and save them to a “wish list.” Because space in their starter home is limited—and because it is a relatively big purchase in their eyes—they decide they need to see the items in person.

Under an optimized cross-channel experience, the couple could find the nearest physical outlet on the retailer’s website, get directions using Google Maps, and drive over to view the desired products. Even before they walk through the doors, a transmitter mounted at the retailer’s entrance identifies Mike and Linda and sends a push alert to their cell phones welcoming them and providing them with personalized offers and recommendations based on their history with the store. In this case, they receive quick links to the wish list they created, as well as updated specs and prices for the washers and dryers that they had shown interest in (captured in their click trails on the store’s website). Additionally, they receive notification of a sale—“15 percent off selected brand appliances, today only”—that applies to two of the items they had added to their wish list.

When they tap on the wish list, the app provides a store map directing Mike and Linda to the appliances section and a “call button” to speak with an expert. They meet with the salesperson, ask some questions, take some measurements, and close in on a particular model and brand of washer and dryer. Because the store employs sophisticated tagging technologies, information about the washer and dryer has automatically been synced with other applications on the couple’s mobile phones—they can scan reviews using their Consumer Reports app, text their parents for advice, ask Facebook friends to weigh in on the purchase, and compare the retailer’s prices against others. Mike and Linda can also take advantage of a “virtual designer” function on the retailer’s mobile app that, with the entry of just a few key pieces of information about room size and decor, allows them to preview how the washer and dryer might look in their home.

All the input is favorable, so the couple decides to take advantage of the 15 percent offer and buy the appliances. They use Mike’s “smartwatch” to authenticate payment. They walk out of the store with a date and time for delivery; a week later, on the designated day, they receive confirmation that a truck is in their area and that they will be texted within a half hour of arrival time—no need to cancel other plans just to wait for the washer and dryer to arrive. Three weeks after that, the couple gets a message from the retailer with offers for other appliances and home-improvement services tailored toward first-year home owners. And the cycle begins again.

… requires new capabilities

As this example makes clear, the forces enabling consumers to expect real-time engagement are unstoppable. Across the entire customer journey, every touchpoint is a brand experience and an opportunity to engage the consumer—and digital touchpoints just keep multiplying. To maximize digital channels, companies need to focus on improving their “3-D” capabilities.

Discover: Build an analytic engine

Even in this era of big data and widespread digitization of customer information, some companies still lack a 360-degree view of the people who buy their products and services. They typically measure the performance of direct sales activities such as product pitches and encourage downloads using “last-action attribution” analyses, which assess campaigns in isolation rather than in the context of the entire cross-channel consumer decision journey. Usually these data will have been stored in disparate locations and legacy systems rather than in a central server. Complicating matters further is the range and quantity of unstructured data out there—information about consumers’ behaviors and preferences that is, for instance, captured in online reviews and social-media posts. In our experience, this type of data is usually the least understood and therefore the least utilized by companies.

To get the full customer portrait rather than just a series of snapshots, companies need a central data mart that combines all the contacts a customer has with a brand: basic consumer data plus information about transactions, browsing history, and customer-service interactions (for an illustrative example of how companies can lose potential customers by failing to optimize digital channels, see exhibit). Tools like Clickfox and Teradata can help marketers gather these data and begin to pinpoint opportunities to engage more effectively with consumers across the decision journey. This collection effort requires input from people across multiple functions—a complex undertaking, to be sure, but the payoff can be big. Our work in this area suggests that the growth rate of earnings before interest, tax, depreciation, and amortization of grocers that focus on customer analytics is 11 percent, compared with just 3 percent on average for their main competitors. For big-box retailers, the difference is 10 percent compared with 2 percent.4

With a comprehensive data set in hand, companies can undertake the sort of quick-hit “shop diagnostics” that many tell us is lacking in their marketing and e-commerce programs. Using analytic applications such as SAS and R, and by applying various algorithms and models to longitudinal data, companies can better model the cost of their marketing efforts, find the most effective journey patterns, spot potential dropout points, and identify new customer segments. Based on its analysis of click-through behaviors, for instance, one regional retailer saw that a particular set of customers preferred digital shopping over physical and always read e-mail on Saturdays, and so the retailer altered its e-mail campaign to send this cohort online offers only on Saturdays.

Additionally, by using business-process software and services from vendors such as Adobe Systems, ExactTarget, Pegasystems, and Responsys, companies can identify in real time the basic “triggers” for what individual customers need and value—regardless of the product or service—and personalize their approach when making cross- or up-sell offers. They can also use these tools to generate automated reports that track customer trends and key performance indicators. For instance, the regional retailer’s analytics suggested that two of the customers who read their e-mail only on Saturdays were in the midst of a career change; both had revised their profiles on LinkedIn within the past three days. Based on its analytics efforts, the company was able to create targeted offers for each—one received information about laptop bags (based on her previous purchases) while the other received information about suits (based on his previous purchases).

Already, the companies employing these types of advanced analytics have seen significantly improved click-through rates and higher conversion rates (between three and ten times the average). Additionally, McKinsey analysis shows that using data to make better marketing decisions can increase marketing productivity by between 15 and 20 percent—that’s as much as $200 billion given the average annual global marketing spend of $1 trillion.5

Design: Create frictionless experiences

Careful orchestration of the consumer decision journey is incredibly complex given the varying expectations, messages, and capabilities associated with each channel. According to published reports, 48 percent of US consumers believe companies need to do a better job of integrating their online and off-line experiences. There is a premium for getting this right. One major bank unlocked more than $300 million in additional margins by making better use of digital channels. It tapped into underutilized customer data and delivered targeted marketing messages at various points in the purchase-decision process. The bank used the data, plus various personalization and testing tools, to inform changes in marketing campaigns for certain product lines; every next step for every customer was progressively tailored to help the customer take the best action.

Digital natives such as Amazon, eBay, and Google have been leading the pack in resetting consumers’ expectations for cross-channel convenience. (Think of eBay’s Now mobile app, which provides one-touch ordering from any of eBay’s retail partners and same-day delivery in some US cities, or Amazon’s recent incorporation of a help button in the company’s latest-generation Kindle Fire tablet, linking users to a live help-desk representative.) These players have perfected the ability to test new user experiences and constantly evolve their offers—often for segments of one.

This lean, start-up approach might sound counterintuitive to large, entrenched marketing organizations in which decisions are made at a snail’s pace, but test-and-learn methods can help companies decide how best to optimize (and customize) critical design attributes of the consumer decision journey at various points along the way. In the appliances example discussed earlier, the retailer’s customer analytics allowed it to design an experience for the couple that was completely customized to their context—from their initial online searches to their physical and virtual interactions at the store and to their follow-up with the company postpurchase. Rather than push what could be construed as intrusive (even creepy) messaging, the retailer provided Mike and Linda with the most useful information at every point in their decision journey and offered the easiest possible path to purchase and delivery.

To create similarly frictionless experiences, some companies have created 24/7 digital “window shops” to test product ideas and customer interactions and collect rapid feedback without the need for additional labor or inventory. Several companies that offer inherently complex products or services have incorporated “gaming” elements into their experiences—tweaking the navigation, content architecture, and visual presentation to allow consumers to trade off and test various options and prices associated with a product before making a decision. One financial-services firm redesigned its mobile app for collecting credit-card applications to incorporate the customer context. Previously it had a one-size-fits-all interface; in the redesigned version, various elements of the mobile app’s interface—such as pricing, stage of process, and designated credit limits—are dynamically generated based on existing customer information. And the app’s page layout and navigation are rendered simply, allowing for easy completion within just a few clicks. The result has been a significant uptick in online applications.

Deliver: Build a more agile organization

In our experience, too many companies are afraid to launch “good enough” campaigns—ones that are continually refined as customers’ purchase behaviors and stated preferences change. Under the direction of conservative senior leaders, teams tend to launch campaigns that take too long to get off the ground and end up revealing few new insights. Instead, they must be willing to conduct lots of small-scale experiments with cloud or proxy website services to pilot new designs and prove their value for investment.

These types of agile, data-driven activities must be supported by an organization that has the right people, tools, and processes. Many companies will have some of the talent required, but not all, and executives will inevitably face resistance when it comes to introducing lean tools and techniques into their sales, marketing, and IT processes. The most successful omnichannel marketers we’ve seen have established centers of excellence in both analytics and digital marketing, and they practice end-to-end management of microcampaigns. Their campaign-building processes typically include systematic calendaring, brainstorming, and evaluation sessions to allow for one-week and two-week turnaround times. And roles and responsibilities are clearly defined. Far from creating a rigid, hierarchical process, this model frees up individuals to iterate quickly—what is sometimes called “failing fast forward” in the world of high tech.

At one bank, for instance, business-unit leaders gather each month to talk about their progress in improving different consumer journeys. As new products and campaigns are launched, the team places a laminated card illustrating the journey at the center of the conference-room table and discusses its assumptions about the flow of the experience for different segments and about how the various functional groups need to contribute: Where does customer data need to be captured and reused later? How will the design of the campaign flow from mass media to social media and then on to the website? What is the follow-up experience once a customer sets up an account? The team has also appointed dedicated mobile and social-media executives to become evangelists for strengthening the omnichannel experience, helping business units raise their game along a range of consumer interactions. The company’s first wave of fixes and new programs generated tens of millions of dollars in the first six months, and the team expects it to continue scaling beyond $100 million in added annual margins.

Building an agile marketing organization will take time, of course. Companies should start by assembling a “scrum team” that will bring the right people together to test, learn, and scale. The team should incorporate cross-functional perspectives (marketing, e-commerce, IT, channel management, finance, and legal), and its members must adopt a war-room mentality—for instance, making tough calls about which campaigns are working and which aren’t, and which messages should take priority for which segments; launching new tests every week rather than every six months; and mustering the IT and design resources to create content for every possible type of interaction.

Companies likely will need to hire people with skills that differ from the ones they rely on now. Some organizations have developed innovative, venture capital–like strategies for finding and recruiting the people they need. Staples, for instance, has built an e-commerce innovation center in Cambridge, Massachusetts, to better recruit technology talent from nearby Harvard University and MIT, and it recently bought conversion-marketing start-up Runa to act as a talent hub on the West Coast.

New types of information systems may also be required. The best technology solutions will vary according to a company’s starting point and objectives. Generally, though, companies will get the best results from tools that enable large-scale data management and the integration of databases; the generation of next-best-action and other types of advanced analyses; and simpler campaign testing, execution, and metrics.

Companies need to make strategic decisions about the best pathways to build customer value. Many cite digital as one of their top three priorities in this regard, but few have taken the time to measure the level of digital maturity their organization has achieved. A company’s digital quotient (DQ) is a function of how well defined its long-term digital strategy is, its effectiveness in implementing that strategy, and the strength of its organizational infrastructure and information technologies. The companies that incorporate the notion of DQ into their short list of performance metrics can more effectively monitor their progress across the digital capabilities we’ve outlined here, enabling more targeted investments and accelerated rates of digital growth.

Indeed, the companies that ultimately succeed in omnichannel marketing and sales will likely resemble tech companies and, interestingly, publishers—effectively using big data and digital touchpoints to drive growth and reduce costs, while producing and managing a variety of content (catalogs, coupons, web pages, mobile apps, and user-generated content) in real time across multiple platforms to create breakthrough customer experiences. This means rethinking the analytics that inform their segmentation strategies, the flow of the experiences they design, and the way they set up their internal operations for faster iteration and delivery of service.